Practice of Internal Auditing

The external auditor has identified a number of production process control deficiencies involving several departments. As a result, senior management has asked the internal audit activity to complete internal control training for all related staff. According to IIA guidance, which of the following would be the most appropriate course of action for the chief audit executive to follow?

A. Refuse to accept the consulting engagement because it would be a violation of independence.

B. Collaborate with the external auditor to ensure the most efficient use of resources.

C. Accept the engagement but hire an external training specialist to provide the necessary expertise.

D. Accept the engagement even if the audit engagement staff was previously responsible for operational areas being trained.

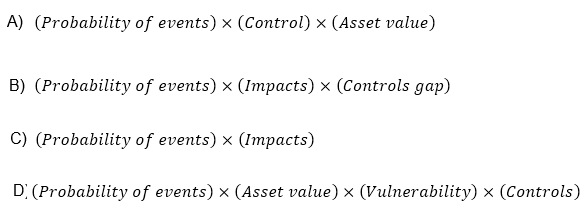

An internal auditor is assessing the organization's risk management framework. Which of

the following formulas should he use to calculate the residual risk?

A. Option A

B. Option B

C. Option C

D. Option D

According to IIA guidance, which of the following strategies would add the least value to the achievement of the internal audit activity's (IAA's) objectives?

A. Align organizational activities to internal audit activities and measure according to the approved IAA performance measures.

B. Establish a periodic review of monitoring and reporting processes to help ensure relevant IAA reporting.

C. Use the results of IAA engagement and advisory reporting to guide current and future internal audit activities.

D. Establish a format and frequency for IAA reporting that is appropriate and aligns with the organization's governance structure.

Due to price risk from the foreign currency purchase of aviation fuel, an airliner has

purchased forward contracts to hedge against fluctuations in the exchange rate. When

recalculating the exchange losses from individual purchases of jet fuel, which of the

following details does the internal auditor need to validate?

1. The hedge documentation designating the hedge.

2. The spot exchange rate on the transaction date.

3. The terms of the forward contract.

4. The amount of fuel purchased.

A. 1 and 2

B. 1 and 4

C. 2 and 3

D. 3 and 4

According to IIA guidance, which of the following are the most important objectives for

helping to ensure the appropriate completion of an engagement?

1. Coordinate audit team members to ensure the efficient execution of all engagement

procedures.

2. Confirm engagement workpapers properly support the observations, recommendations,

and conclusions.

3. Provide structured learning opportunities for engagement auditors when possible.

4. Ensure engagement objectives are reviewed for satisfactory achievement and are

documented properly.

A. 1, 2, and 3

B. 1, 2, and 4

C. 1, 3, and 4

D. 2, 3, and 4

A chief audit executive (CAE) is determining which engagements to include on the annual audit plan. She would like to consider the organization's attitude toward risk and the degree of difficulty in achieving objectives. Which of the following resources should the CAE consult?

A. The corporate risk register.

B. The strategic plan.

C. Internal and external audit reports.

D. The board's meeting records.

During an assurance engagement, an internal auditor noted that the time staff spent accessing customer information in large Excel spreadsheets could be reduced significantly through the use of macros. The auditor would like to train staff on how to use the macros. Which of the following is the most appropriate course of action for the internal auditor to take?

A. The auditor must not perform the training, because any task to improve the business process could impact audit independence.

B. The auditor must create a new, separate consulting engagement with the business process owner prior to performing the improvement task.

C. The auditor should get permission to extend the current engagement, and with the process owner's approval, perform the improvement task.

D. The auditor may proceed with the improvement task without obtaining formal approval, because the task is voluntary and not time-intensive.

Due to a recent system upgrade, an audit is planned to test the payroll process. Which of the following audit objectives would be most important to prevent fraud?

A. Verify that amounts are correct.

B. Verify that payments are on time.

C. Verify that recipients are valid employees.

D. Verify that benefits deductions are accurate.

When constructing a staffing schedule for the internal audit activity (IAA), which of the

following criteria are most important for the chief audit executive to consider for the

effective use of audit resources?

1. The competency and qualifications of the audit staff for specific assignments.

2. The effectiveness of IAA staff performance measures.

3. The number of training hours received by staff auditors compared to the budget.

4. The geographical dispersion of audit staff across the organization.

A. 1 and 3

B. 1 and 4

C. 2 and 3

D. 2 and 4

When establishing a quality assurance and improvement program, the chief audit executive

should ensure the program is designed to accomplish which of the following objectives?

1. Add value.

2. Improve operations.

3. Provide assurance that the internal audit activity conforms with the Standards.

4. Provide assurance that the internal audit activity conforms with the IIA Code of Ethics.

A. 1 only

B. 1 and 2 only

C. 1 and 3 only

D. 1, 2, 3, and 4

During an audit of the accounts receivable (AR) process, an internal auditor noted that reconciliations are still not performed regularly by the AR staff, a recommendation that was made following a previous audit. Monitoring by the financial reporting function has failed to detect the shortcoming. Both the financial reporting function and AR report to the controller, who is responsible for implementing action plans. Which of the following supports the internal auditor's decision to combine both observations into one reported finding?

A. The observation was made during the same audit, and the action plan has a common owner.

B. The observation relates to the same control activity within a common process.

C. The observation has a common control, and it was noted in a prior audit.

D. The observation has a common process, and the action plan for the observation has a common owner.

According to IIA guidance, which of the following is true regarding the exit conference for an internal audit engagement?

A. A primary purpose of the exit conference is to provide for the timely communication of observations that call for immediate management action.

B. Both the chief audit executive and the chief executive over the activity or function reviewed must attend the exit conference to validate the findings.

C. The exit conference provides only anticipated results for inclusion in the final audit communication.

D. During the exit conference, the performance of the internal auditors who executed the engagement is reviewed.

| Page 19 out of 51 Pages |

| 11121314151617181920212223242526 |

| IIA-ACCA Practice Test Home |

Real-World Scenario Mastery: Our IIA-ACCA practice exam don't just test definitions. They present you with the same complex, scenario-based problems you'll encounter on the actual exam.

Strategic Weakness Identification: Each practice session reveals exactly where you stand. Discover which domains need more attention, before ACCA CIA Challenge Exam exam day arrives.

Confidence Through Familiarity: There's no substitute for knowing what to expect. When you've worked through our comprehensive IIA-ACCA practice exam questions pool covering all topics, the real exam feels like just another practice session.

Copyright © All Rights Reserved