Your client Jerry's asset mix is deviating from the original target asset mix because the stock market has had strong performance. Equities are now over-weighted in Jerry's account. The original target asset mix is still valid since Jerry's situation has not changed. He is invested in several bond and equity mutual funds. What should you do?

A. advise him to change his know your client (KYC) form to reflect more growth

B. advise him to do nothing since equities could outperform bonds in the next year

C. advise him to sell a portion of assets invested in bond funds and reinvest the proceeds into equity funds

D. advise him to sell a portion of assets invested in equity funds and reinvest the proceeds into bond funds

Explanation:

According to the Canadian Investment Funds Course, asset mix rebalancing

is the process of restoring the portfolio to its original or target asset allocation by selling or

buying assets. Asset mix rebalancing is necessary to maintain the desired level of risk and

return, as well as to align the portfolio with the investor’s objectives and circumstances.

Asset mix rebalancing can be done periodically, such as annually or quarterly, or based on

a threshold, such as when an asset class deviates from its target weight by a certain

percentage.

In this case, Jerry’s asset mix is deviating from the original target asset mix because the

stock market has had strong performance. Equities are now over-weighted in Jerry’s

account. The original target asset mix is still valid since Jerry’s situation has not changed.

He is invested in several bond and equity mutual funds. Therefore, the best course of

action is to advise him to sell a portion of assets invested in equity funds and reinvest the

proceeds into bond funds. This will bring his portfolio back to its target asset mix and

reduce his exposure to equity risk.

The other options are not advisable because:

The owners of Underground Airways Ltd. want to take their privately owned corporation public through an initial public offering (IPO). They are speaking to a specialist from an investment dealer to determine whether it would be advisable to become listed on a stock exchange or the over-the counter (OTC) market. In comparing the two options, which of the following considerations is TRUE?

A. Underground would be subject to less stringent listing requirements if they chose the stock exchange as compared to the OTC market.

B. If Underground chose to list on the OTC market, there would be no secondary market available for investors.

C. Underground would still be directly involved in the trading of their shares on either market.

D. A stock exchange listing would provide Underground with greater market exposure and public confidence than listing on the OTC market.

Explanation:

According to the Canadian Investment Funds Course, a stock exchange is a

centralized and regulated market where securities of listed companies are traded between

buyers and sellers. A stock exchange has strict listing requirements that companies must

meet in order to be eligible for trading on the exchange. These requirements may include

minimum capitalization, number of shareholders, financial reporting, corporate governance,

and compliance with securities laws. A stock exchange also provides liquidity,

transparency, and efficiency for the trading of securities.

An over-the-counter (OTC) market is a decentralized and unregulated market where

securities that are not listed on a stock exchange are traded between dealers and brokers.

An OTC market has no physical location, rather the trading is done through phone, email,

or computer networks. An OTC market has lower listing requirements than a stock

exchange, which makes it easier for smaller or newer companies to access capital.

However, an OTC market also has less liquidity, transparency, and efficiency than a stock

exchange.

Therefore, if Underground Airways Ltd. wants to take their privately owned corporation

public through an initial public offering (IPO), they would have to weigh the pros and cons

of listing on a stock exchange or the OTC market. One of the main considerations is that a

stock exchange listing would provide them with greater market exposure and public

confidence than listing on the OTC market. This is because a stock exchange listing

signals that the company has met the high standards of the exchange and is subject to

ongoing regulation and oversight. A stock exchange listing also attracts more investors,

analysts, and media attention than an OTC listing. A stock exchange listing may also

increase the value and liquidity of the company’s shares.

Which of the following CORRECTLY describes a material conflict of interest that has been properly addressed by the Dealing Representative?

A. Cametra asks to meet with her client, Pietro, to update his Know Your Client (KYC) information. They have not had a face-to-face meeting in years. Pietro feels updating the KYC information is unnecessary. He tells Cametra he is too busy and there is no reason for her to be concerned with the information she already has. Even though they fail to meet, Cametra continues to submit purchase orders at his request.

B. Gibson reviews two similar mutual funds for his client. One fund pays higher trailer fees than the other. Gibson discloses the difference between the trailer fees before recommending the fund that has higher trailer fees.

C. Keaira recommends a growth fund to her client, Shilo, but her Compliance Department questions the trade because Shilo's risk profile is too low. Rather than cancel the trade and absorb the market losses herself, Keaira recommends that Shilo keep the investment even though it is not in her best interest. Keaira updates Shilo's KYC to "high" risk and gets Shilo to sign the KYC update form.

D. Oscar wants to recommend a fund to his client which has a higher management expense ratio (MER) than other mutual funds. Since the MER could impact the client's decision, Oscar reports the conflict of interest to his dealer and discloses the conflict of interest to his client. Oscar explains how the higher MER is in the client's best interest because the overall cost for the client will still be less than a fee-for-service account holding mutual funds with a lower MER.

Explanation: A material conflict of interest is a situation where a Dealing Representative or their firm has an interest that could reasonably be expected to affect the exercise of their professional judgment or influence their actions or recommendations. A Dealing Representative must identify, disclose, and manage any material conflicts of interest in the best interest of their clients. Oscar has properly addressed the material conflict of interest arising from the higher MER by reporting it to his dealer, disclosing it to his client, and explaining how it is in the client’s best interest. The other scenarios do not demonstrate proper management of material conflicts of interest.

Ellen and her only son Jeff live on the family farm with her father George. Jeff is five years old and Ellen has decided that it is time to start saving for Jeff’s post-secondary education. She has called you to ask about registered education savings plans (RESPs). Which of the following statements is TRUE?

A. If Jeff qualifies for additional CESG. his CESG lifetime maximum increases to $10,000.

B. If Jeff decides not to pursue a post-secondary education, he can keep all the CESG but it then becomes taxable.

C. George may open an RESP for Jeff but it will not quality to receive Canada Savings Education Grants (CESGs).

D. If Ellen receives the National Child Benefit Supplement (NCBS), Jeff may be eligible for the Canada Learning Bond

Explanation: If Ellen receives the National Child Benefit Supplement (NCBS), Jeff may be eligible for the Canada Learning Bond (CLB). The CLB is a grant of up to $2,000 that the Government of Canada deposits into a child’s RESP to help low-income families start saving for their child’s education2. The CLB does not require any contributions from the parents. To be eligible for the CLB, the child must have been born after December 31, 2003 and the family must receive the NCBS, which is part of the Canada Child Benefit3. The other statements are false. If Jeff qualifies for additional CESG, his CESG lifetime maximum increases to $7,200, not $10,000. If Jeff decides not to pursue a post-secondary education, he cannot keep the CESG; it must be returned to the government. George may open an RESP for Jeff and it will qualify to receive CESGs, as long as George is a resident of Canada and has a valid social insurance number.

Solomon is a Dealing Representative who is excited about a new equity fund his dealer recently approved. He thinks investors will be attracted to the fund’s historical performance. He has a prospective new client, Madira, who is 25 years old. Madira has invested in mutual funds before, but not with Solomon’s dealer. She has made an appointment to open a new RRSP with Solomon’s firm. What does Solomon need to do to make this a suitable recommendation?

A. Show from past fund performance, that mutual fund costs are not important if there are high returns.

B. Rely on the risk rating of the mutual fund when offering an investment solution.

C. Identify how the proposed investment is in alignment with the investor's profile and holdings.

D. Match the past rates of return of the mutual fund with what is the anticipated rate of return.

Explanation: To make a suitable recommendation, Solomon needs to identify how the proposed investment is in alignment with the investor’s profile and holdings. A suitable recommendation is one that meets the investor’s needs, goals, risk tolerance, time horizon, and personal circumstances. It also considers the investor’s existing portfolio and how the new investment would affect its diversification, performance, and risk. Therefore, option C is correct regarding what Solomon needs to do to make a suitable recommendation. The other options are not correct or sufficient to make a suitable recommendation. Option A is false because mutual fund costs are important regardless of the past fund performance, as they reduce the net returns and compound over time. Option B is false because relying on the risk rating of the mutual fund is not enough to offer an investment solution, as it does not reflect the investor’s return expectations, liquidity needs, tax situation, or personal preferences. Option D is false because matching the past rates of return of the mutual fund with what is the anticipated rate of return is not a reliable way to make a recommendation, as past performance does not guarantee future results and may not be consistent with the investor’s risk tolerance or time horizon.

When you buy a put option, which of the following is TRUE?

A. You have the right to sell a set number of shares at a set price.

B. You have the right to purchase a set number of shares at a set price.

C. You have the obligation to sell a set number of shares at a set price.

D. You have the obligation to buy a set number of shares at a set price.

Explanation: A put option is a contract that gives the buyer the right, but not the obligation, to sell a set number of shares of an underlying asset at a set price within a specified time frame. The buyer of a put option expects the price of the underlying asset to fall below the strike price before the expiration date. Therefore, A is the correct answer.

Which of the following Dealing Representatives has CORRECTLY fulfilled their suitability obligation?

A. Clarence determines that the Absolute Alternative Fund is suitable for all of his clients. Clarence believes that all investors need alternative funds in order to be properly diversified.

B. Kiri recommends the Conservative Bond Fund to his client, Myrtle. The fund generates income and Myrtle's investment objective is "income" on her Know Your Client (KYC) form.

C. Li Ming recommends the Venturex Labour-Sponsored Fund to her client, Park. While Park has low tolerance and capacity for risk, Li Ming provides detailed disclosure which explains the fund's risks.

D. Roderik determines that the model portfolio he has developed will be suitable for all of his clients. Roderik has included investments with both income and growth to appeal to all investors.

Explanation: Kiri has correctly fulfilled his suitability obligation by matching the risk-return profile of the fund with the personal circumstances of his client. The Conservative Bond Fund is a low-risk, low-return fund that pays regular interest income to investors. Myrtle’s investment objective is “income”, which means she wants to receive steady income from her investments and preserve her capital. Therefore, Kiri’s recommendation is reasonably suitable for Myrtle in all the circumstances. (Canadian Investment Funds Course, Chapter 2, Section 2.3)

What trait or characteristic is normally associated with a person who would be designated as a Trusted Contact Person (TCP)?

A. Normally has a financial interest in the client's account or assets.

B. Often involved with providing care for the client who requires personal assistance.

C. Has the authority to make financial decisions on behalf of the client.

D. Can simplify difficult financial concepts for the client.

Explanation: A Trusted Contact Person (TCP) is someone who the client authorizes their financial advisor to contact in limited circumstances, such as when the client is vulnerable, has a health issue, or cannot be reached. A TCP should be someone who the client trusts and who is mature and can handle difficult conversations about the client’s personal situation. Often, a TCP is someone who is involved with providing care for the client who requires personal assistance, such as a family member, a friend, or a caregiver. A TCP does not have a financial interest in the client’s account or assets, does not have the authority to make financial decisions on behalf of the client, and does not need to simplify financial concepts for the client.

Which of the following is a characteristic of a bond fund?

A. Income from a bond fund will primarily be interest but may also be capital gains

B. Bond funds are very low risk because they never go down in value.

C. If interest rates rise the value of a bond fund will also tend to rise.

D. Securities regulation specifies that bond funds must invest in investment grade bonds.

Explanation: A bond fund is a mutual fund that invests primarily in bonds and other debt securities. Income from a bond fund will primarily be interest but may also be capital gains if the fund sells bonds that have appreciated in value. Bond funds are not very low risk because they can fluctuate in value depending on interest rate changes and credit risk. If interest rates rise, the value of a bond fund will tend to fall because existing bonds will become less attractive than new bonds with higher rates. Securities regulation does not specify that bond funds must invest in investment grade bonds, although some funds may have this as an investment objective or policy.

Which of the following statements about registered education savings plans (RESPs) is CORRECT?

A. Contributions to RESPs are tax deductible.

B. There is a yearly contribution limit per beneficiary.

C. RESPs must be collapsed by the end of the 31st year of its starting date

D. Contributed funds grow tax-free within the plan.

Explanation: Contributed funds grow tax-free within the plan3. This means that any income or capital gains earned by the investments in an RESP are not taxed until they are withdrawn3. This allows the plan to grow faster than a taxable account with the same investments and contributions3. The other statements are incorrect. Contributions to RESPs are not tax deductible3. This means that you cannot deduct the amount you contribute to an RESP from your taxable income3. However, you do not have to pay tax on the contributions when they are withdrawn from the plan3. There is no yearly contribution limit per beneficiary, but there is a lifetime contribution limit of $50,000 per beneficiary3. This means that you can contribute any amount to an RESP in any given year, as long as you do not exceed the lifetime limit for each beneficiary3. RESPs must be collapsed by the end of the 35th year of its starting date3. This means that you have up to 35 years to use the funds in an RESP for educational purposes or transfer them to another plan3. If you do not use or transfer the funds by then, you have to close the plan and pay tax on the accumulated income portion3.

What statement CORRECTLY describes a key difference between bonds and debentures?

A. Regular secured bonds offer a higher level of income than debentures.

B. Bonds are secured by the specific assets of a company whereas debentures are not secured by real assets or collateral.

C. Debentures have higher priority than bondholders for the company's assets in the event that the company goes bankrupt.

D. Debentures are considered high risk because they are not backed by the reputation or credit worthiness of the issuer.

Explanation: Bonds and debentures are both types of debt instruments that can be issued by corporations or governments to raise capital. However, they differ in the way they are secured. Bonds are backed by the specific assets of the issuer, such as property, equipment, or inventory. This means that if the issuer defaults on the bond payments, the bondholders have a claim on those assets and can sell them to recover their money. Debentures, on the other hand, are not secured by any real assets or collateral. They are only backed by the general creditworthiness and reputation of the issuer. This means that if the issuer defaults on the debenture payments, the debenture holders have no recourse to any specific assets and have to rely on the issuer’s ability to pay from its future earnings or liquidation proceeds.

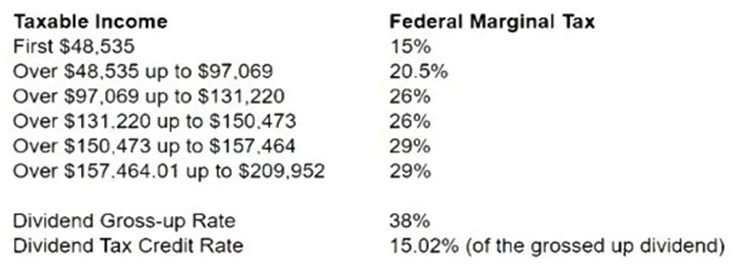

Last year Peter’s earned income from employment was $50,000.

Last year, after receiving a $2 per share in dividends from 500 shares in ABC Inc., a

publicly-traded Canadian corporation, he sold his shares. The sale resulted in a capital gain

of $15,000.

Based on the tax rates mentioned above, what is Peter’s net federal tax liability for the

year? (Round to 2 decimal places).

A. $9,953.30

B. $9,193.69

C. $9,113.53

D. $9,696.15

Explanation: To calculate Peter’s net federal tax liability for the year, we need to follow

these steps:

Step 1: Calculate Peter’s taxable income. This is the amount of income that is

subject to federal income tax. It is equal to his earned income from employment

plus his net capital gain plus his grossed-up dividend income. A net capital gain is

50% of the capital gain realized from selling an asset. A grossed-up dividend

income is the actual dividend received plus a percentage of the dividend that

reflects the corporate tax paid by the issuer. According to the image, the dividend

gross-up rate is 15.02%. Therefore, Peter’s taxable income is:

50000+0.5×15000+(500×2)×(1+0.1502)=68251.00

Step 2: Apply the federal tax rates to Peter’s taxable income according to the tax

brackets shown in the image. The federal tax rates are progressive, meaning that

higher income is taxed at higher rates. Therefore, Peter’s federal tax before credits

is:

0.15×(485350)+0.205×(6825148535)=11293.69

Step 3: Subtract the federal tax credits from Peter’s federal tax before credits. A

tax credit is an amount that reduces the tax payable by a taxpayer. There are two

types of federal tax credits: non-refundable and refundable. Non-refundable tax

credits can only reduce the tax payable to zero, but not below zero. Refundable

tax credits can reduce the tax payable below zero, resulting in a refund to the

taxpayer. In this question, we assume that Peter only has two non-refundable tax

credits: the basic personal amount and the dividend tax credit.

The basic personal

amount is a fixed amount that every taxpayer can claim to reduce their taxable

income. According to this site, the basic personal amount for 2021 is $13,808. The

dividend tax credit is a percentage of the grossed-up dividend income that reflects

the corporate tax paid by the issuer and avoids double taxation. According to this

site, the federal dividend tax credit rate for eligible dividends in 2021 is 15.0198%.

Therefore, Peter’s federal tax credits are:

0.15×13808+0.150198×(500×2)×0.1502=2100

Step 4: Subtract Peter’s federal tax credits from his federal tax before credits to get

his net federal tax liability. This is the amount of federal income tax that Peter has

to pay or has overpaid for the year. Therefore, Peter’s net federal tax liability is:

11293.692100=9193.69

Hence, option B is correct.

| Page 7 out of 19 Pages |

| 456789 |

| CIFC Practice Test Home |

Real-World Scenario Mastery: Our CIFC practice exam don't just test definitions. They present you with the same complex, scenario-based problems you'll encounter on the actual exam.

Strategic Weakness Identification: Each practice session reveals exactly where you stand. Discover which domains need more attention, before Canadian Investment Funds Course Exam exam day arrives.

Confidence Through Familiarity: There's no substitute for knowing what to expect. When you've worked through our comprehensive CIFC practice exam questions pool covering all topics, the real exam feels like just another practice session.

Copyright © All Rights Reserved